Our primary mission is to assess or valuate the financial value of your intangible assets. We also support you in your asset valorization or monetization processes.

The assessment of the financial value of intangible assets is essential in various economic and commercial contexts. Here are some examples:

• Fundraising or Financing →

Context: A company may need to assess its intangible assets to convince investors of their value during a fundraising round or to secure financing.

Example: A start-up developing innovative technology assesses its patents to justify a high valuation to venture capital investors.

• Sales or Licensing Transactions →

Context: When a company sells or licenses an intangible asset, such as a trademark or patent, it must assess its value to set an appropriate sale price or license fee.

Example: A micromechanics company selling a license for a new engine must assess the value of this license based on expected future revenues.

• Calculation of Royalties or Franchise Payments →

Context: In franchise or licensing agreements, companies must assess the value of intangible assets to determine the amount of royalties to be received or paid.

Example: A restaurant chain assesses the value of its brand and culinary expertise to set the royalties paid by franchisees.

• Strategic Planning and Internal Management →

Context: Assessing intangible assets enables company leaders to make informed decisions regarding the development, optimization, or disposal of these assets.

Example: A fashion company assesses the value of its brands to decide on international expansion or to determine whether a new marketing campaign is justified.

• Periodic Reevaluation for Strategic Needs →

Context: Regular reassessment of intangible assets allows companies to adapt to market changes and adjust their strategies accordingly.

Example: A micromechanics company reassesses the value of its new engine license to ensure it reflects the projected future revenues.

• Mergers and Acquisitions →

Context: When a company considers merging with or acquiring another company, it is essential to evaluate the latter's intangible assets, such as trademarks, patents, or goodwill, to determine a fair purchase price (Fair value).

Example: A technology company evaluates the patents of a start-up before acquiring it to determine whether these patents justify the asking price.

• Product Development or Innovation →

Context: Before investing in the development of new products or technologies, companies must assess the value of their existing intangible assets to ensure the investment is justified.

Example: A high-tech company assesses the value of its patents and expertise before deciding to invest in R&D for a new generation of products.

Development of innovative products

• Partnerships or Joint Ventures →

Context: When forming partnerships or joint ventures, assessing intangible assets helps partners determine each party's contribution and equitably share profits.

Example: Two companies—one in mechanics and the other in electronics—creating a joint venture to develop a new product, assess their patents and technologies to define each party’s equity share.

• Litigation and Arbitration →

Context: In disputes involving intellectual property rights or commercial contracts, assessing intangible assets is crucial for determining damages or resolving conflicts.

Example: A company sues a competitor for patent infringement and must assess the financial value of the patent in question to claim damages.

• Collaterals (Guarantees, Pledging) →

Context: Intangible assets can be used as collateral to obtain financing, especially for companies with limited physical assets or whose value is primarily based on intellectual property.

Example: Start-ups, often rich in intellectual property but lacking physical assets, use their patents as collateral to secure growth financing.

An entertainment company uses its copyrights and trademarks as guarantees to raise funds for new projects.

A biotechnology company uses its patents on developing drugs as collateral to finance clinical trials or bring the product to market.

Note: The use of intellectual property (IP) as collateral in loans or financing is a growing field.

• Market Consolidation →

Context: When a company seeks to consolidate its position in a specific market, it may assess its intangible assets to identify opportunities for organic growth or acquisitions.

Example: A beverage industry giant assesses the value of its local brands to decide whether a branding campaign or regional acquisition is the best way to consolidate its market share.

• Risk Management and Compliance →

Context: Companies often need to evaluate the value of their intangible assets as part of risk management and regulatory compliance, particularly to ensure they meet data protection or intellectual property standards.

Example: A cybersecurity company assesses the value of its encryption technologies to ensure compliance with legal requirements and evaluate financial risk in the event of a security breach.

• Restructuring or Liquidation →

Context: In the event of financial restructuring or liquidation, intangible assets must be assessed to maximize recoveries for creditors or redistribute assets.

Example: In the case of a company's bankruptcy, its intangible assets, such as trademarks or software, are assessed for auction.

• Asset Transfers During Internal Reorganization →

Context: When a company restructures its divisions or transfers assets between internal legal entities, assessing intangible assets is necessary to ensure fair and compliant distribution.

Example: An international company transfers patents from its European subsidiary to the parent company in the United States and must assess their value to comply with tax regulations.

• Preparing for an Initial Public Offering (IPO) →

Context: Before an initial public offering (IPO), a company must assess its intangible assets to present a clear and attractive valuation to potential investors.

Example: A software company assesses its goodwill, customer base, and intellectual property rights to set its share price for the IPO.

• Financial Reporting and Accounting →

Context: Companies often need to assess their intangible assets to include them in their financial statements, particularly during acquisitions or when updating the book value of these assets.

Example: A software company includes the value of its software portfolio in its balance sheet after a revaluation due to the obsolescence of some licenses.

Context: When calculating taxes, assessing the value of intangible assets is necessary, particularly for tax depreciation or tax declarations during asset transfers.

Example: A company transferring patents to a foreign subsidiary must assess these patents to calculate the taxes on the transfer.

• Internal Audit and Management Control →

Context: Internal auditors may need to assess intangible assets to ensure proper management, protection, and optimal use within the company.

Example: A multinational company conducts an audit of its intellectual property rights in several subsidiaries to verify compliance and efficient use.

• Insurance of Intangible Assets →

Context: Some companies purchase insurance policies for their intangible assets, such as patents or trademarks. A prior assessment is necessary to determine appropriate coverage and premiums.

Example: An entertainment company assesses the value of its copyrights and trademarks before taking out insurance to protect them from potential losses due to infringement.

• Stock Options or Profit-Sharing Plans →

Context: When issuing stock options or profit-sharing plans for employees, companies often need to assess their intangible assets to determine the overall valuation of the company.

Example: A start-up assesses the value of its patent portfolio before determining the value of stock options granted to its key researchers.

• Succession or Estate Planning →

Context: Family business owners may need to assess their intangible assets to organize succession or plan the transfer of their estate.

Example: A family business owner assesses the value of the brand and know-how passed down from generation to generation to plan the succession.

In each of these contexts, the valuation of intangible assets is essential for making informed financial decisions and ensuring that all parties involved receive a fair economic value.

Several methods are used to estimate the financial value of intangible assets. Each method is suited to different types of assets and contexts. Below is an overview of the main valuation methods.

The cost approach estimates the value of an asset based on the costs incurred to create it.

Historical Cost Method: This method is based on the actual costs incurred to create or acquire the asset (e.g., development or acquisition costs). It is straightforward but may not reflect the current value of the asset.

Replacement Cost Method: The value is estimated based on the cost required to recreate or replace the intangible asset. This includes development, protection (e.g., patents, copyrights), and commercialization costs.

Reproduction Cost Method: Similar to the replacement cost method, but assumes an exact reproduction of the asset, including any imperfections or specific features.

Comparable Transactions Method: The asset is valued by comparing it to recent transactions involving similar assets under comparable market conditions. This method is useful for assets with established markets, such as trademarks or patents.

Market Multiples Method: Financial ratios from similar transactions, such as revenue or profit multiples, are used to estimate the asset’s value. This method is often applied to entire companies but can also be used for specific intangible assets.

Discounted Cash Flow (DCF) Method: The asset is valued by estimating the future cash flows it will generate and discounting them at the expected rate of return to obtain the present value. This is a commonly used method for patents, trademarks, and other intangible assets.

Excess Earnings Method: The value is calculated by determining the excess earnings generated by the asset, after subtracting earnings attributed to tangible assets.

Relief-from-Royalty Method: The value is estimated by calculating the royalties that would have been paid if the company had needed to license the asset. This method is commonly used for brands and copyrights.

Real Options Method: This approach integrates elements from both income and market methods, considering the flexibility and uncertainties associated with the asset. It is useful for evaluating assets with high potential future value, like emerging technologies.

Goodwill Method: Primarily used in mergers and acquisitions, this method estimates goodwill by comparing the company’s purchase price to the value of its tangible and identifiable assets. The difference represents the value of intangibles like reputation and brand.

Evaluating intangible assets requires careful selection of the most appropriate method, depending on the nature of the asset, the availability of data, and the objectives of the valuation. Each method has its advantages and limitations, and in some cases, multiple methods may be used together to obtain a more accurate estimate of financial value.

By relying on robust data, various valuation methods, rigorous risk modeling, the use of mathematical tools, and professional expertise, it is possible to achieve a valuation that is as precise and reliable as possible, thus providing a solid foundation for financial decision-making.

The Income Approach, being the most commonly used (and often criticized), deserves to be explored in more detail.

Valuing Intangible Assets: An "Educated Guess"?

Valuing intangible assets such as patents, trademarks, or goodwill—especially with the cost approach—is often referred to as an "educated guess" due to the inherently uncertain and subjective nature of these assets. Unlike physical assets, intangible assets lack easily measurable intrinsic value, making their valuation complex.

a. What is the Reality?

Intangible Nature: Intangible assets lack physical substance, and their value is based on perceptions, future cash flow expectations, or strategic advantages. For example, a brand’s value depends on consumer loyalty, reputation, and market positioning, which are difficult to quantify precisely.

Multiple Uncertainties: Valuing intangible assets involves uncertainties, including the future revenues the asset may generate, its economic lifespan, market changes, and legal or competitive risks. Each of these variables can significantly impact the estimated value.

Lack of Comparables: Unlike physical assets like machines or buildings, intangible assets are often unique, and comparable transactions are rare, complicating valuation.

Subjective Factors: Valuation often involves subjective judgments, such as estimating brand awareness, the strength of customer relationships or the impact of a patented innovation. While based on experience, these judgments are open to interpretation.

b. How to Improve the Reliability of the Valuation?

Collecting Comprehensive and Reliable Data:

Historical Data Analysis: Gathering accurate data on the asset’s past performance, such as revenue generated by a patent or brand, is crucial. This includes analyzing past cash flows, operating costs, and growth trends.

Searching for Comparables: Even though comparables are rare, it is essential to seek similar transactions or assets within the industry to provide a reference framework.

Using Multiple Valuation Methods:

Income, Market, and Cost Approaches: By combining these approaches, a range of possible values can be obtained, reducing uncertainties.

Sensitivity Analysis: Testing key assumptions (e.g., growth rates, royalty rates, or discount rates) helps understand how changes in these parameters affect the estimated value.

c. Risk and Uncertainty Modeling:

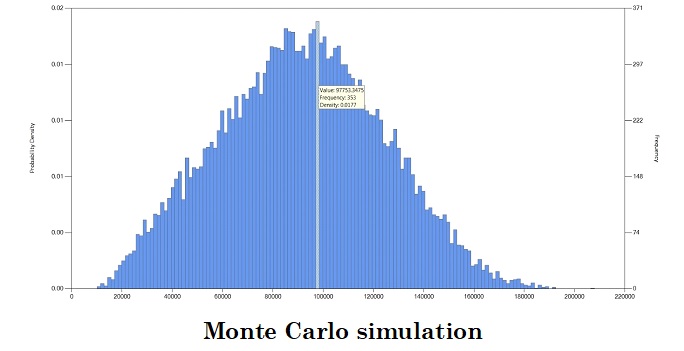

Monte Carlo Simulation: This technique models uncertainties and risks related to future cash flows. It generates a distribution of potential values rather than a single estimate, offering a more comprehensive view of risk.

Scenario Analysis: Developing optimistic, pessimistic, and most likely scenarios helps capture a range of outcomes based on different risk factors.

d. Consulting Experts and Professional Judgment:

Engaging Experts: Collaborating with specialists in intellectual property, branding, or specific industries enriches the valuation process with expert insights.

e. Documentation and Transparency:

Clarity on Assumptions: Clearly document all assumptions used in the valuation, including justifications for the chosen methods and data.

Transparency on Uncertainties: Communicating uncertainty levels and risk factors associated with the estimate allows for more informed decision-making.

This structured approach helps improve the reliability of intangible asset valuations, ensuring that decisions are based on thorough analysis and professional judgment.

Monte Carlo Simulation in Financial Valuation of Intangible Assets

Monte Carlo simulation is a statistical method used to model uncertainty and variability in complex processes, particularly valuable in the financial valuation of intangible assets such as patents, trademarks, or copyrights. This approach helps estimate an asset’s value by considering the many uncertain factors that can affect its future profitability.

a. Principle of Monte Carlo Simulation

Monte Carlo simulation models the probability distribution of possible outcomes by running repeated simulations. Unlike a single deterministic estimate, this method explores a wide range of potential scenarios by performing multiple simulations based on random variables.

This method involves the following steps:

Qualitative Analysis of Patents - Kiviat Diagram

Identification of Key Variables: Begin by identifying the uncertain variables that influence the intangible asset’s value. These may include revenue growth rates, royalty rates, future costs, asset lifespan, technological risks, market risks, and discount rates.

Definition of Probability Distributions: Assign a probability distribution to each variable, representing the range of potential values it can take and their likelihood. For instance, future revenues of a brand might be modeled using a normal distribution around a mean value with a given variance.

Random Simulation: Conduct numerous simulations (often in the thousands) by randomly generating values for each variable based on their respective distributions. For each simulation, calculate the intangible asset's value based on the generated values.

Analysis of Results: After completing all simulations, a distribution of potential values for the intangible asset is produced. This distribution provides insight into not only the average or median value but also the associated risks, such as extreme outcomes or value percentiles.

b. Advantages of Monte Carlo Simulation

Incorporation of Uncertainty: Monte Carlo simulation explicitly accounts for the inherent uncertainty in key variables such as cash flow forecasts, providing a more comprehensive view of risk.

Multiple Scenarios: Instead of relying on a single or limited number of deterministic scenarios, this method explores a broad spectrum of possible outcomes. This is especially useful for intangible assets, where the value depends on highly unpredictable factors.

Risk Quantification: The resulting distribution of asset values allows for quantifying the risk associated with the asset. Metrics such as the probability of exceeding or falling below a certain value threshold can be easily identified.

c. Applications in Valuation of Intangible Assets

Patent Valuation: Monte Carlo simulation can model potential future revenues from patent licenses, considering uncertainties like the patent’s lifespan, technological adoption, and market dynamics.

Brand Valuation: For brand valuation, the simulation can incorporate uncertainties related to consumer trends, market shifts, and branding strategy effectiveness.

Goodwill Analysis: In acquisitions, this method can assess the value of goodwill by simulating different market conditions and their impact on the company’s future profits.

d. Conclusion

Monte Carlo simulation is a robust tool for valuing intangible assets, capturing the uncertainty and variability of the factors influencing their value. By generating a complete distribution of possible asset values, it enables decision-makers to better understand the risks involved and make more informed financial decisions.

The key steps in the financial valuation of intangible assets include:

a. Identification of Intangible Assets

The initial step is to precisely identify the intangible assets that need to be valued. This involves determining which assets have an identifiable economic value and can be separated from the company for individual assessment. Common examples include patents, trademarks, copyrights, trade secrets, goodwill, customer relationships, and know-how.

b. Analysis of the Asset's Specific Characteristics

Each intangible asset possesses unique characteristics that can influence its valuation. For example:

Duration: The legal and economic lifespan of the asset (such as the protection period of a patent) plays a crucial role in determining its value.

Geographic Scope: The asset’s geographic coverage (for example, a trademark registered in multiple countries) can impact its valuation.

Level of Legal Protection: The strength and extent of the legal protection associated with the asset significantly influence its value.

c. Choice of One or More Valuation Methods

The selection of an appropriate valuation method depends on the nature of the intangible asset. Common approaches include:

i. Market Approach

This method involves comparing the intangible asset to recent transactions involving similar assets. It relies on the availability of comparable data and is particularly useful for common intangible assets like trademarks or copyrights in industries with frequent transactions.

ii. Income Approach

This approach values the asset based on the future revenue it is expected to generate. Often used for patents or technologies, it projects future cash flows and discounts them at an appropriate rate to determine the asset’s net present value. This method also accounts for risks like market fluctuations or competition.

iii. Cost Approach

The cost approach estimates the value of an intangible asset by calculating the costs associated with its creation or replacement. This includes development, reproduction, or replacement costs. While straightforward, it may not reflect the current market value but can be useful when other methods are impractical.

d. Consideration of Risks and Uncertainty

Valuation must also account for the risks and uncertainties associated with intangible assets. These can include:

Legal Risks: Such as potential litigation.

Market Risks: Such as the risk of technological obsolescence.

Operational Risks: Including commercial failure.

Advanced techniques like Monte Carlo simulations can model these uncertainties, providing a more robust and reliable estimate of the asset’s value.

e. Economic and Strategic Context

Valuation must also consider the economic and strategic environment in which the asset is used. This involves assessing market trends, the company’s competitive position, and how the asset fits into the company’s overall strategy. The value of an intangible asset can vary depending on the context of its utilization.

f. Conclusion

Valuing intangible assets requires a combination of methods, each providing unique insights. By analyzing the asset’s specific characteristics, employing market, income, or cost-based approaches, and factoring in risks and strategic context, a reliable estimate of value can be obtained.

The product is a safety device designed for the elderly, with a patent filed and granted in Switzerland. A business plan has been developed based on market research to explore its potential.

Evaluation of intangible assets protecting the invention

b. Purpose of the Valuation

The purpose of the valuation is to assess the financial value of the Swiss patent.

c. Objective of the Valuation

The primary objective is to enable the inventor to engage with potential investors and secure funding for finalizing and commercializing the product.

d. Critical Analysis of the Business Plan

The business plan undergoes a detailed analysis to verify its plausibility and realism. In the case of any inconsistencies or unclear points, the inventor is consulted to clarify these issues. A "revised" version of the business plan, reflecting these clarifications, is used for the valuation.

e. Patent Analysis

A qualitative review of the patent is conducted, focusing on several aspects:

Technical Scope: Assessing the actual protection the patent confers in terms of technology.

Geographic Scope: Evaluating the patent’s coverage, noting that it is only valid in Switzerland.

Lifespan: Considering how much time remains before the patent expires.

Competitive Landscape: Identifying competing products and analyzing the potential for the patent to be circumvented.

f. Risk Analysis

A risk assessment is carried out, typically in collaboration with the project owner, addressing both technical and commercial risks that could affect the patent’s value.

g. Discount Rate Evaluation

The discount rate is evaluated by considering the various factors that influence it, such as market conditions, risk levels, and the project’s financial forecasts.

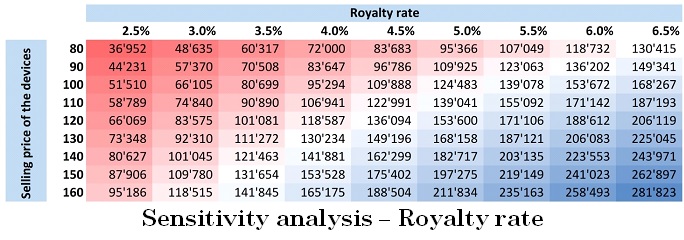

h. Sensitivity Analysis

Sensitivity Analysis

A sensitivity analysis is performed to identify the parameters that have the most significant impact on the patent’s final value. This helps to pinpoint which variables are crucial to monitor closely.

i. Monte Carlo Simulation

For each parameter influencing the patent’s value, a probability curve is defined (typically characterized by a mean value and standard deviation). These curves serve as input data for a Monte Carlo simulation. A large number of trials (e.g., 20,000) are run to generate a probability distribution of the patent’s value.

j. Final Result

The most likely value derived from the Monte Carlo simulation is considered the patent's estimated value. Alternatively, a range can be presented, defined by the mean value and the interquartile range, to reflect the uncertainty and variability in the patent's valuation.

A standard valuation report for the financial value of intangible assets is a detailed document that outlines the results of an analysis aimed at estimating the value of these assets. It is designed to be thorough yet understandable for a range of stakeholders, including investors, executives, or auditors. The main sections typically found in such a report are as follows:

Valuation Report

a. Introduction

Context and Objective of the Valuation: This section explains the purpose of the valuation, such as for mergers and acquisitions, fundraising, or asset sales, along with the specific objectives guiding the valuation process.

Description of Intangible Assets: Provides a clear identification of the intangible assets being valued, including patents, trademarks, goodwill, or other relevant assets. It describes their nature, role within the company, and their strategic importance.

b. Valuation Methodology

Approaches Used: This section details the valuation methods applied, such as the income approach, market approach, or cost approach, with a rationale for selecting each method based on the characteristics of the assets being valued.

Key Assumptions: A summary of the key assumptions underpinning the valuation, including projections of revenue growth, asset lifespan, royalty rates, replacement costs, and discount rates.

Data Sources: Identifies the sources of data used in the valuation, which may include financial reports, market studies, historical financial performance, and industry benchmarks.

c. Analysis of Intangible Assets

Asset Characteristics: A detailed evaluation of the specific characteristics of each intangible asset, such as its legal protection, remaining lifespan, geographic coverage, and its contribution to company performance.

Market Study: An analysis of the economic environment and competitive landscape in which the asset operates. This includes data on market trends, industry dynamics, and the company's competitive position within the sector.

d. Valuation Results

Estimated Value: Presents the results of the valuation for each intangible asset, noting the values derived from the different valuation methods. Any differences between the values from different methods are explained.

Sensitivity Analysis: An examination of how changes in key assumptions (e.g., revenue growth rates or discount rates) affect the estimated value of the asset.

Alternative Scenarios: Explores the value of the asset under various scenarios, such as optimistic, pessimistic, and base cases, to assess the impact of different assumptions on the final valuation.

e. Conclusions and Recommendations

Monte Carlo Simulation

Summary of Results: A concise summary of the main conclusions of the valuation, highlighting which assets are most valuable and identifying the key factors that influence their value.

Strategic Recommendations: Provides guidance on actions to take based on the valuation results. This could include strategies for protecting or enhancing the value of the asset, monetization options, or recommendations for managing associated risks.

Limitations of the Valuation: Outlines the limitations of the analysis, addressing uncertainties related to market conditions, speculative assumptions, or constraints in data availability.

f. Appendices

Detailed Data: Inclusion of tables, charts, and detailed calculations used in the valuation process.

Reference Documents: References to source documents, market studies, financial reports, or any other material used to inform the valuation.

Expert CVs: Presentation of the qualifications and experience of the experts who conducted the valuation, to establish the credibility of the report.

g. Certifications and Declarations

Independence Declaration: A statement certifying that the valuation was conducted independently and without conflicts of interest.

Compliance Certification: Confirms that the valuation process adhered to current accounting and valuation standards and practices, ensuring the analysis meets professional guidelines.

A standard valuation report of intangible assets is a comprehensive and structured document that offers a well-supported estimate of an asset's value. It serves as a solid foundation for strategic decision-making and ensures transparency, rigor, and credibility in the valuation process.

Photo by Bastian Riccardi on

Unsplash

Photo by Bastian Riccardi on

Unsplash